Table of Contents

- Cross Market Sports Arbitrage Trading

- Trading Strategy 1: A Cross

- 3 1 Algorithmic Strategies In Agent Trading

- Moving Average Price Crossing Trading Strategy: Es Day Trade

- Live Trading With Dttw On Youtube

- Design Of The Market

Robinhood is the broker for traders who want a simple, easy-to-understand layout without all the bells and whistles other brokers offer. Though its trading options and account types are limited, even an absolute beginner can quickly master Robinhood’s intuitive and streamlined platform. On the other hand, more advanced traders might be frustrated by Robinhood’s lack of technical analysis tools, a feature that’s now nearly universal across other platforms.

What is invisible trade?

Invisible trade refers to an international transaction which does not involve tangible goods, but services, such as consultancy services, insurance, banking, intellectual property, international tourism, etc. In other words, it is the import and export of services between countries.

Table3 shows the experimental results.Footnote 6 The results indicate that although some groups’ results are not significant, the last group is significant. This means the wealth growth rate differs among the four types of investors, and the effectiveness of the four trading strategies is therefore different. Specifically, the informed investment strategy is optimal; it is the only one that can increase the investor’s wealth. The second is the technical trading strategy, which ultimately does not increase investor wealth; it did, however, offer opportunities for profit in the simulation experiment. The third is the arbitrage trading strategy; its average wealth growth rate is negative, but it offers a chance for profit through arbitrage.

Cross Market Sports Arbitrage Trading

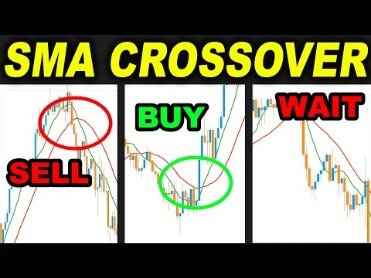

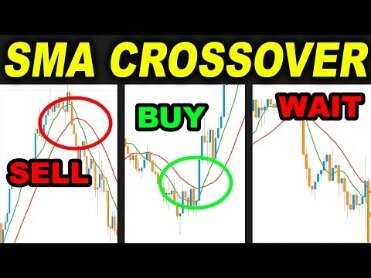

The style of trading can have a substantial impact on any trading system. A system that performs well on daily charts might not perform as well when run as a day trade or shorter term swing trade. Most day-trading algorithms have a larger number of trades and because they hold for a shorter duration, they typically have smaller average gain/trades. This was discussed earlier, and is when the price crosses above or below a moving average to signal a potential change in trend. On the chart below, we have used a 15-day and 25-day moving average, which is a popular combination among day traders. However, since the 50-day and 200-day moving averages are relatively wide for day traders, most of them have narrowed down the periods. Some will combine the 10 and 50-period moving averages while others will combine the 25-period and 50-period MAs.

A different pattern emerges when we compare trading activity across substantially different highly active markets, underscoring the fact that the cross-market activity measure is not simply picking up spurious coactivity. Overall, the large share of cross-market activity probably helps explain the extremely tight link between Treasury cash and futures markets. Consistent with this, the two highest volatility days in October 2014, the 15th and 16th, also had the most cross-market activity. For common exchange members that are not members of FINRA, the member’s Designated Examining Authority (“DEA”) serves as the examining authority and DCSA. For the purpose of this study, we will be analyzing this strategy in the context of a Longer Term Swing Trading.

Prior to CAT, there was no single, comprehensive audit trail available to regulators. The SROs however, use a variety of data sources, including the EBS and, through the ISG forum, data from the COATS and ECAT, the ISG’s equity audit trail, to help fulfill their regulatory obligations. In addition, FINRA has had the ability to collect cross-market data through the Order Audit Trail System (“OATS”). OATS is a system operated by FINRA which compiles information reported by member firms.

Trading Strategy 1: A Cross

The best day trading research platforms for you will depend upon the trading strategy you plan on using and which market you intend to employ it in. Another key way to prepare yourself for day trading consists of obtaining the knowledge about the fundamental market moving factors that drive the financial markets you intend to trade. Although once primarily practiced by professionals, day trading has become increasingly popular with retail traders who wish to speculate in the financial markets for their own account. The relatively recent advent of online trading platforms and brokers that support them has given rise to a new generation of day traders eager to profit from market fluctuations. Among the first who analyzed algorithmic trading pattern in electronic order books, Prix et al. studied changes in the lifetime of cancelled orders in the XETRA order book. Owing to the characteristics of their data set, they are able to identify each order by a unique identifier and so re create the whole history of events for each order. Gsell and Gomber likewise focus on differences in trading pattern between human and computer-based traders.

Each trading strategy consists of multiple confluence factors to provide robust signals. Of course, one can add more triggers and criteria to this approach. If you like this approach and are interested in learning my current trading strategies and get my trade setups, make sure to check our Masterclass where we currently have a special deal. Let’s talk about trading strategies and in this article, I am sharing 5 trading strategies that I use or have used in my own trading.

If the price of gold goes up, the profitability of gold miners should increase, also. If the gold price increases quickly, either the gold miner’s stock prices must follow, or the gold price must fall. Statistical arbitrage uses statistics and mathematical models to profit from relationships between financial instruments. Victoria “V.E.” Schwab is the bestselling author of more than a dozen books, including Vicious, the Shades of Magic series, and This Savage Song. Her latest novel, The Invisible Life of Addie LaRue, is BuzzFeed Book Club’s December pick. Lucy Foley is the New York Times bestselling author of the thrillers The Guest List and The Hunting Party.

3 1 Algorithmic Strategies In Agent Trading

As shown in Table4, the average capital occupation of the arbitrage strategy is 3.43E+ 05, and the average capital occupation of the other three strategies is 5.28E+ 04. Thus, the capital occupation of arbitrage traders is nearly 6.5 times that of other investors, which means arbitrage traders do indeed need more capital. We obtain 60,522 period data for the occupation of capital among all trading strategies.

While the model breaking down is the primary risk, there are many risks with each type of statistical arbitrage. Pairs trading is one of the many types of statistical arbitrage.

- As I mentioned above, I’m not particularly eager to pair trade stocks.

- This is the worst case for all analysis done utilizing this trading strategy.

- We follow Johnson’s proposal by illustrating the chronology of algorithm development.

- In order to read or download sports arbitrage advanced series cross market trading strategies ii ebook, you need to create a FREE account.

Traders often have differing priorities when selecting a broker depending on their level of experience and trading activity level. You will want to select a broker suitable for your particular needs and preferences. Smart order routing technology in the new European equity trading landscape.

Moving Average Price Crossing Trading Strategy: Es Day Trade

Repeat the trade from step # 5, as many times as necessary, until your daily profit target has been reached, or until your market is no longer active, or no longer moving decisively. Add a 50 bar CCI, a 25 bar CCI, and a 34 bar exponential moving average of the HLC typical price (calculated as (High + Low + Close) / 3)). He is a professional financial trader in a variety of European, U.S., and Asian markets. Research examining high-frequency exchange rate data has found that mispricings do occur in the foreign exchange market such that executable triangular arbitrage opportunities appear possible. In observations of triangular arbitrage, the constituent exchange rates have exhibited strong correlation. Triangular arbitrage opportunities may only exist when a bank’s quoted exchange rate is not equal to the market’s implicit cross exchange rate. The following equation represents the calculation of an implicit cross exchange rate, the exchange rate one would expect in the market as implied from the ratio of two currencies other than the base currency.

Then, when the price manages to move above the 200 moving average, more buyers get convinced that this is, indeed, a bull run and then continue pushing the price higher. This is a bullish signal that emerges when two moving averages make a crossover. The most common periods of the two moving averages are 50-day and 200-day moving averages.

Statistical Arbitrage strategies can be applied to different financial instruments and markets. The Executive Programme in Algorithmic Trading includes a session on “Statistical Arbitrage and Pairs Trading” as part of the “Strategies” module. Many of our EPAT participants have successfully built pairs trading strategies during their course work. A number of providers offer online day trading chat room platforms where traders can discuss and exchange trade ideas with each other on a timely basis.

Why do you need 25k to day trade?

Brokerage firms wanted an effective cushion against margin calls, which led to the increased equity requirement. The money must be in your account before you do any day trades and you must maintain a minimum balance of $25,000 in your brokerage account at all times while day trading.

For the purpose of this study, we will be analyzing this strategy when applied to market indexes. We will apply a robust quantitative analysis in order to confirm or deny the popular Moving Average Price Crossing Strategy. We will also attempt to separate fact from fiction with regard to various “tips and techniques” related to the Moving Average Price Crossover trading system. The material is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Because each instrument is traded in multiple venues, a trader has to monitor liquidity and price levels in each venue in real time. Automated, algorithm-based low-latency systems provide solutions in fragmented markets. Smart order routing engines monitor multiple liquidity pools to identify the highest liquidity and optimal price by applying algorithms to optimize order execution. They continuously gather real-time data from the respective venues concerning the available order book situations (Ende et al. 2009). Foucault and Menkveld analyze executions among two trading venues for Dutch equities and argue that suboptimal trade executions result from a lack of automation of routing decisions. Ende et al. empirically assess the value of SOR algorithms in a post-MiFID fragmented European securities system. They find suboptimal executed trades worth €262 billion within a four-week data set.

Nevertheless, the importance of such automated safeguards has risen in the eyes of regulators on both side of the Atlantic. A more critical view of algorithmic trading is provided by researchers from the London-based Foresight Project. The authors illustrate possible liquidity or price shock cascades, which also intensified the U.S. This hypothesis is backed, in part, by Zhang and Kirilenko et al. , each finding HFT to be highly correlated with volatility and the unusually large selling pressure noted during the Flash Crash. Among the theoretical evidence on the benefits of algorithmic trading, the model presented by Foucault et al. achieved significant attention. In order to determine the benefits and costs of monitoring activities of securities markets, the authors develop a model of trading with imperfect monitoring to study this trade-off and its impact on the trading rate.

The prevailing negative opinion about algorithmic trading, especially HFT, is driven in part by media reports that are not always well informed and impartial. Most of the scientific literature credits algorithmic trading with beneficial effects on market quality, liquidity, and transaction costs. Only a few papers highlight possible risks imposed by the greatly increased trading speed. However, all academics encourage objective assessments as well as sound regulation in order to prevent system failures without cutting technological innovation. This section concentrates on major findings regarding the U.S. and European trading landscape as it concerns. Impact, on trade modification and cancellation rates, market liquidity, and market volatility. Permanent market observation and quantitative models make up only one pillar essential to both kinds of arbitrage.

It’s by trading these types of techniques that professionals make so much money on a regular basis. Day trading tends to suit attentive individuals capable of managing the stress of intense risk-taking activity. Successful day traders will typically be more experienced market operators who have traded for several years and have the right personality type to deal calmly and objectively with the volatility often seen in the financial markets. Some market analysts and traders put a limited amount of reliance on the death cross pattern because it is often a very lagging indicator. The downside moving average crossover may not occur until significantly after the point at which the trend has shifted from bullish to bearish.

This phenomenon is the reason why market impact costs make up one part of the implicit trading costs (Harris 2003; Domowitz and Yegerman 2005). Impact-driven algorithms seek to minimize the effect that trading has on the asset’s price. By splitting orders in to sub-orders and spreading their submission over time, these algorithms characteristically process sub-orders on the basis of a predefined price, time, or volume benchmark. The volume-weighted average price benchmark focuses on previous traded prices relative to the order’s volume. The overall turnover divided by the total volume of the order sizes indicates the average price of the given time interval and may represent the benchmark for the measurement of the performance of the algorithm. Focusing on execution time, the time-weighted average price benchmark algorithm generate—in its simplest implementation—equally large sub-orders and processes them in equally distributed time intervals. Trading intervals can be calculated from the total quantity, the start (p. 321)time, and the end time; for example, an order to buy 120,000 shares in chunks of 5,000 shares from 10 o’clock to 12 o’clock, results in five-minute trading intervals.

“They’re perfectly valid, but people treat them all as individual trades rather than being part of a system. You can’t pick one and then when it doesn’t work say ‘so much for that’. It’s an absurd thing for short-term traders and business TV to take notice of,” said Boorman. In contrast, Jon Boorman sees golden crosses as good trading indicators. This brings us to the next important step that we need to establish for our long-term trading strategy, which is where to place our protective stop loss. The second half of our position is entered once we break and close below the 200-day moving average.